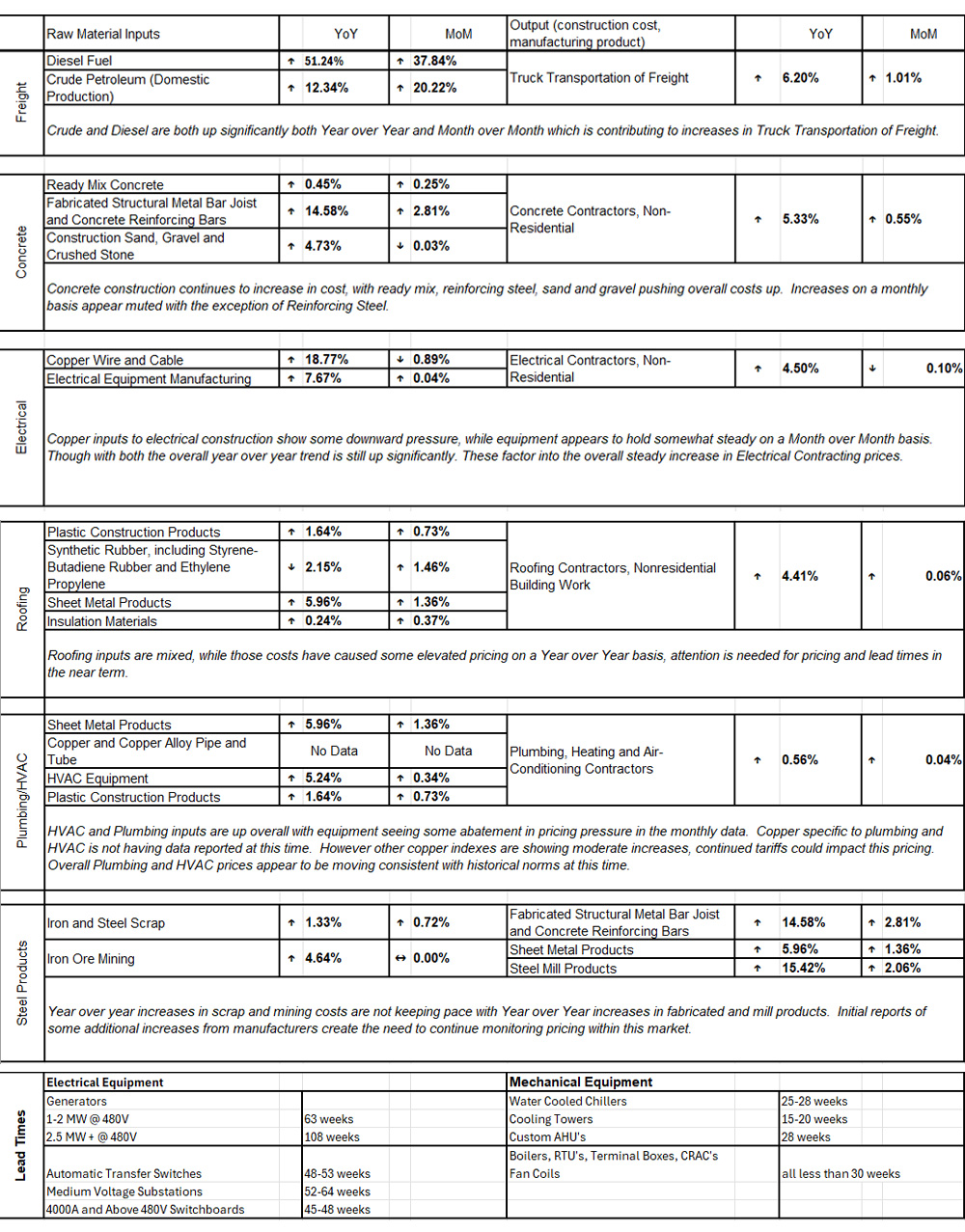

Market and material pricing is accelerating upward across the board. Current Lead time information for major Electrical and Mechanical Equipment is shown below. For detailed information and longer-term trends please see the graphs and charts above. There are three different views for materials and commodities and please continue to note the labor market information on the 4th tab. Use the arrows at the bottom of the charts to switch between views and use the drop-down menu to navigate between products and commodities.

Other notes:

- Overall month over month changes in March indicate continued inflation pressures.

- Final construction costs continue to have upward pressure.

- Labor continues to be a pressure in certain markets. Regional pressures will continue in labor markets as large manufacturing, infrastructure and healthcare projects ramp up. These labor pressures will increase final construction costs on large, longer duration projects as contractors include labor escalators to manage risks.

- Even though the pace of wage increases has slowed it is still trending at the upper end of historical averages year-over-year, with national wages up 5.03% year-over-year